11 Practical Saving Money Tips For Teens

You want to keep cash for things that matter, not impulse buys or late fees.

Small steps matter more than dramatic plans.

These tips are practical, tested, and easy to start this week.

11 Practical Saving Money Tips For Teens

These 11 strategies are written for real life and ready to try. Each one is actionable and focused on habits you can start now.

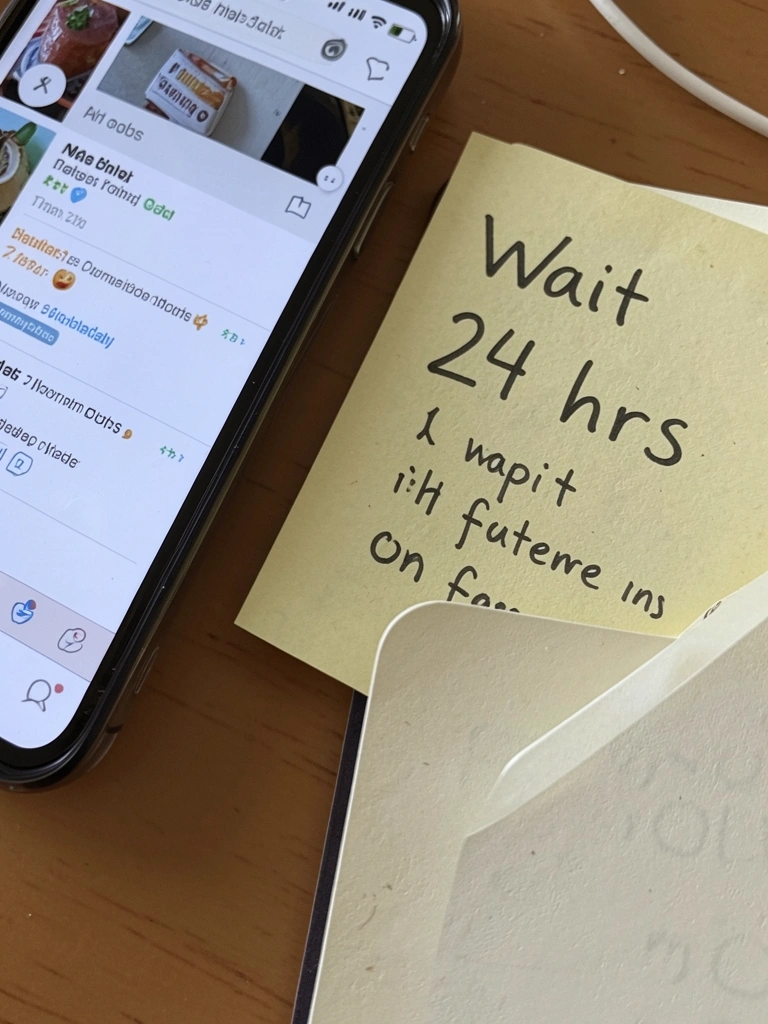

1. The 24-Hour Rule That Stops Impulse Spending

When you want something nonessential, wait 24 hours before buying. That pause drops impulse buys because desire often fades after a day.

When you try this, put the item on a “maybe” list and set a reminder. If it still matters after a day, consider saving for it or using part of your spending money.

A common mistake is bypassing the rule by telling yourself “just this once.” Catch that thought, and move the money into savings instead of checkout.

Tip: use a note app or a paper list so the decision is tracked, not emotional.

2. Automate Small Round-Up Savings

Set up automatic transfers that round purchases up to the nearest dollar or move a small fixed amount after each payday. It turns saving into a background habit.

You’ll barely notice the money missing, but a few dollars per week compounds quickly into a clear fund for trips or gadgets.

Watch out for accounts with fees; automation is only worth it if the transfers aren’t eaten by charges.

Tip: start with an amount you won’t feel. If $1 per purchase feels tight, try a weekly $5 transfer instead.

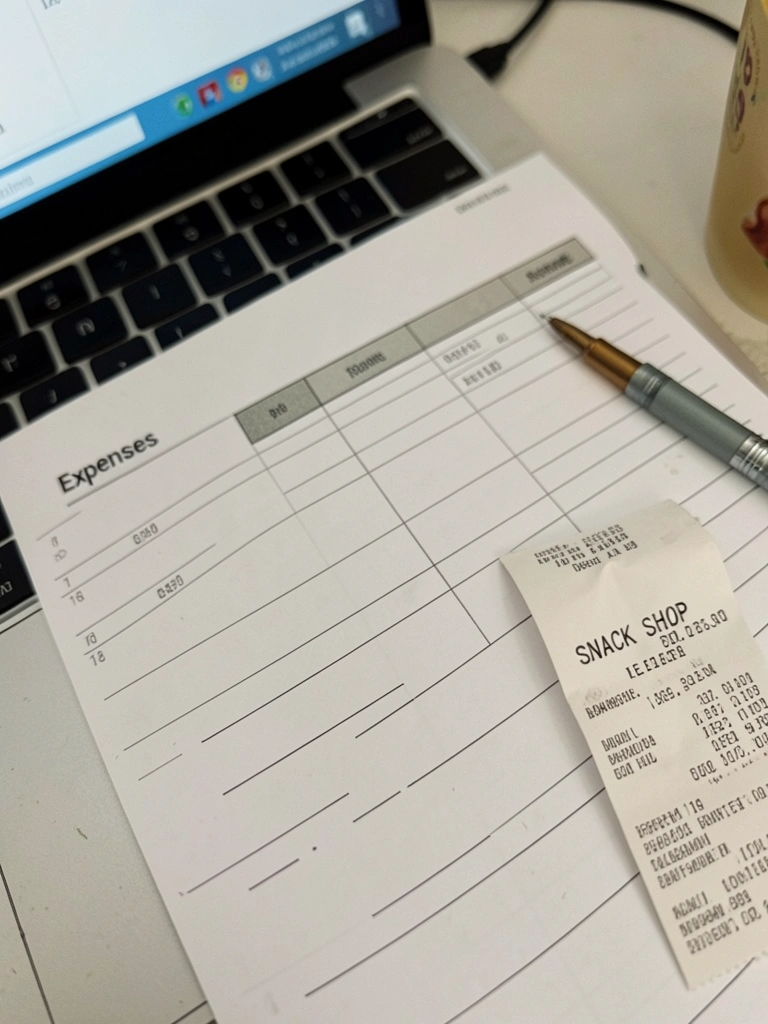

3. Track Every Expense for 30 Days

Write down every purchase for 30 days, even a $1 candy bar. Tracking reveals where money leaks — rideshares, snacks, subscriptions — that feel small but add up.

When you see totals, pick one quick cut to free up cash: skip two rideshares a week or make drinks at home. That gives immediate cash to save.

A common pitfall is stopping after a week because it feels tedious; consistency reveals patterns that one week hides.

Tip: use a simple notes app or one-column spreadsheet; clarity beats perfect categories.

4. Save for One Short-Term Goal at a Time

Pick one clear goal — a phone, concert ticket, or weekend trip — and decide the target amount and date. Breaking it into weekly portions makes the math painless.

You’ll know exactly how much to set aside from each paycheck or allowance. That clarity reduces random spending because the goal is visible.

A mistake is juggling too many goals at once, which makes progress feel invisible. Focus on one goal for a few months, then start the next.

Tip: name the goal and give it a physical place, like a jar or a sub-savings account.

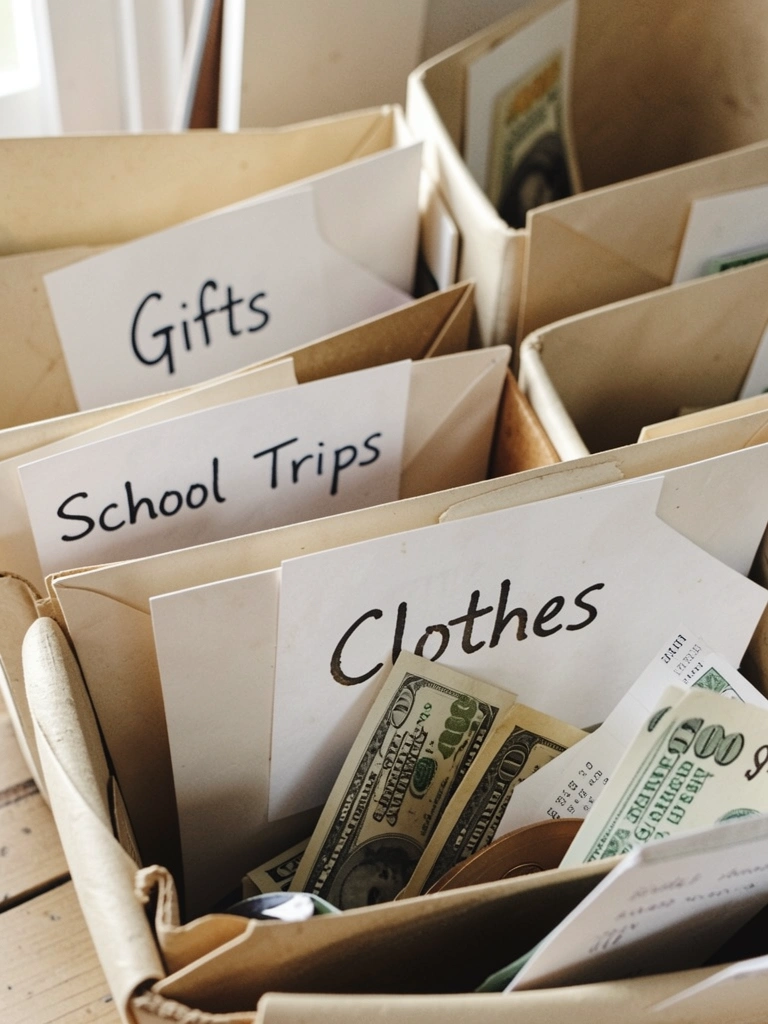

5. Use Sinking Funds for Irregular Costs

Instead of being surprised by occasional expenses, set up small sinking funds. Decide what comes up yearly — gifts, trips, or shoes — and divide that cost into monthly saves.

This changes how money feels: irregular bills stop derailing your monthly budget because the cash is already there.

Avoid the trap of calling it “extra” and spending it early. Keep sinking funds separate from everyday spending so they stay reserved.

Tip: use a divided wallet, separate savings jars, or a labeled sub-account at your bank.

6. Split Income Into Clear Buckets

When you get paid, immediately divide it into at least three parts: short-term savings, spending money, and long-term savings or giving. Decide percentages that fit your life.

This forces intentional choices: the spending bucket controls day-to-day choices, while savings buckets grow without decision fatigue.

A common error is using “leftover” as a plan. Don’t wait to see what remains; allocate up front.

Tip: start with an easy split like 50% spend, 30% save, 20% long-term or adjust to match your needs.

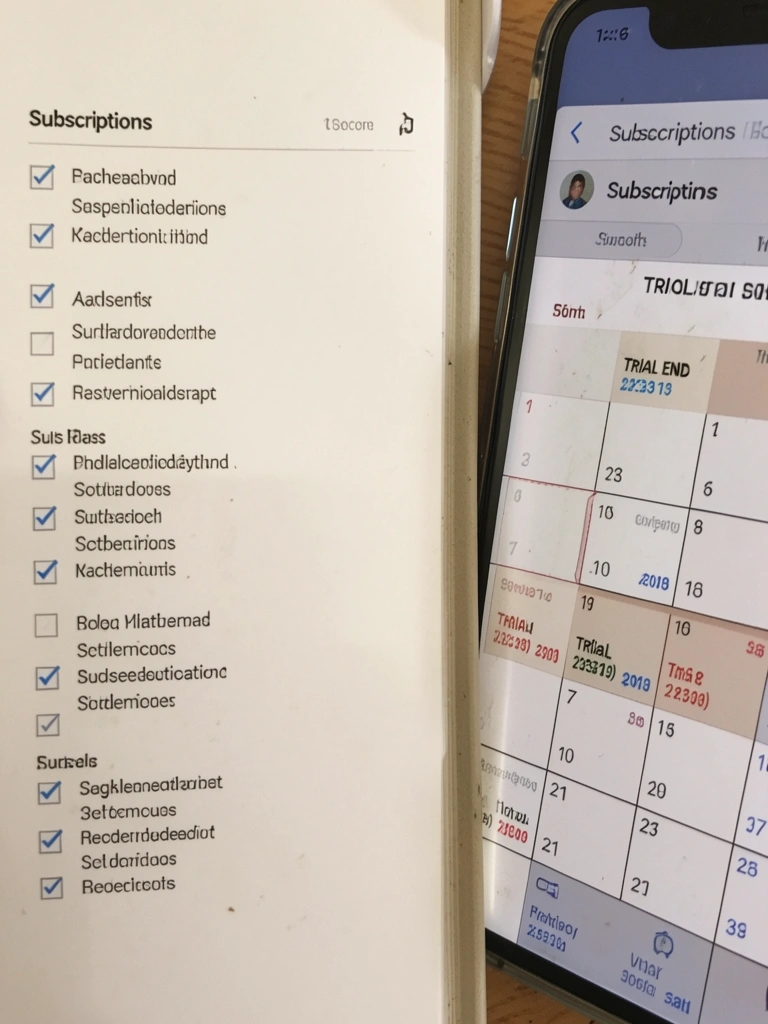

7. Cancel Unused Subscriptions and Trials

Scan your accounts for recurring charges and free trials set to auto-renew. Cancel anything you don’t use regularly; those $5–$10 monthly fees add up fast.

You’ll free money without changing habits. The key is regular checks — once every two months is enough to catch surprises.

A pitfall is forgetting free trials and being billed later. Use calendar alerts when starting new trials so cancellations are on time.

Tip: group subscriptions in one place and evaluate which ones give real value.

8. Negotiate or Share Costs for Bigger Bills

If a phone plan or streaming fee is in your name, ask for student discounts or move to a family shared plan. Sharing costs with family members or splitting services reduces what you pay.

Negotiation works: ask for discounts, lower tiers, or bundled options. If you’re honest about what you use, providers often offer simpler, cheaper plans.

Don’t accidentally downgrade to a plan that misses essentials; compare features before switching.

Tip: prepare the facts — current bill, usage, and competitor prices — then make a calm ask.

9. Turn One Hobby Into a Tiny Side Income

If you enjoy making things, tutoring, or tech help, set a modest price and sell a few hours a month. Route all earnings straight into savings so side income builds a fund.

You’ll learn how to price time and see direct results from effort. Keep scope small — one product or service — so it doesn’t burn you out.

A common mistake is underpricing or mixing side income with spending. Track hours and treat it like a mini business at first.

Tip: start with friends and family to build confidence and save rather than spend the first checks.

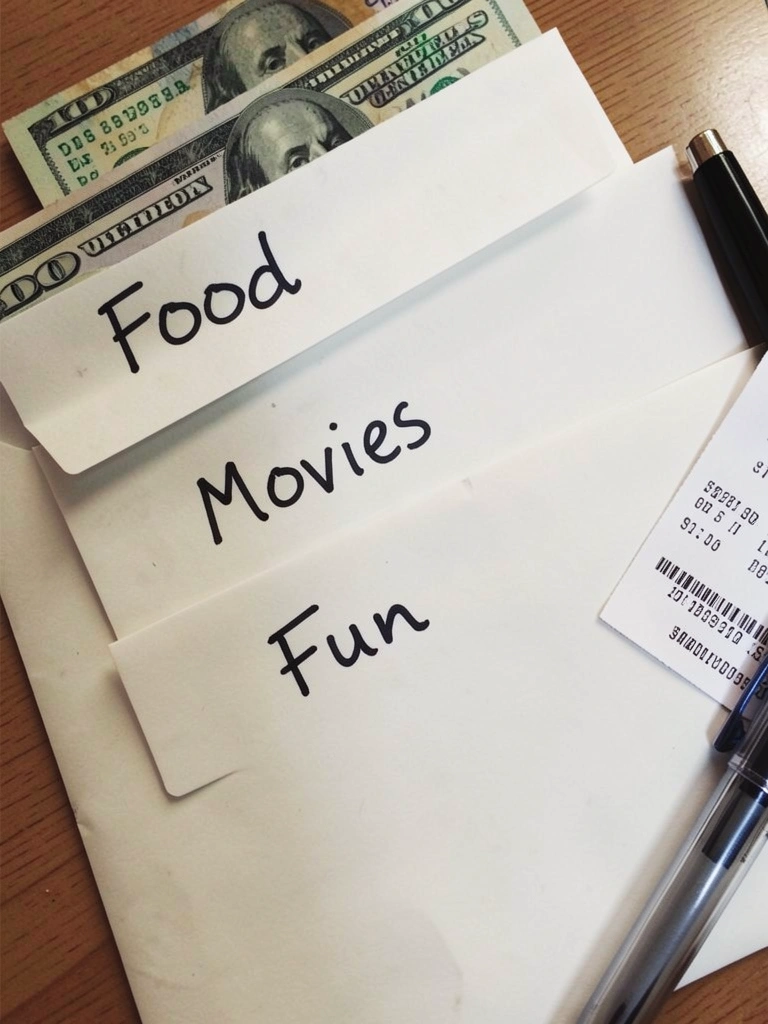

10. Use Cash Envelopes for Discretionary Spending

Allocate a set amount of cash each week for nonessentials and keep it in envelopes. When the envelope is empty, that category is done for the week.

You’ll feel the limit physically, which curbs overspending faster than cards. It also builds awareness of how quickly small purchases add up.

A pitfall is “borrowing” from another envelope and never paying it back. Treat each envelope as its own account.

Tip: combine envelopes with a simple notes app to record what spent and why.

11. Avoid Bank Fees and Understand Interest Basics

Choose accounts that don’t charge monthly maintenance or ATM fees and stay within withdrawal limits. Fees can quietly eat your small balances.

Understand that savings grow faster with accounts offering higher returns, and fees reduce that growth. You don’t need complex math — just avoid obvious charges and watch the balance trend up.

Don’t assume a low balance is fine; some accounts penalize small balances. Check terms and pick an account that fits how you use money.

Tip: keep an eye on statements monthly so surprises are caught early.

Final Thoughts

You don’t have to do every tip at once. Pick two that fit your routine and stick with them for a month.

Small, consistent changes build a real habit. Keep going, and your options will expand without stress.