How To Pay Off Credit Cards Efficiently

You feel the weight of credit card bills stacking up and emails about due dates keep popping up.

You want a clear plan that actually reduces balances, not a to-do list that sits unread.

You need a step-by-step way to stop interest from growing and get visible progress in your accounts.

How To Pay Off Credit Cards Efficiently

This shows a practical path to reduce balances, avoid missed payments, and free up budget room over time. The steps are achievable and repeatable.

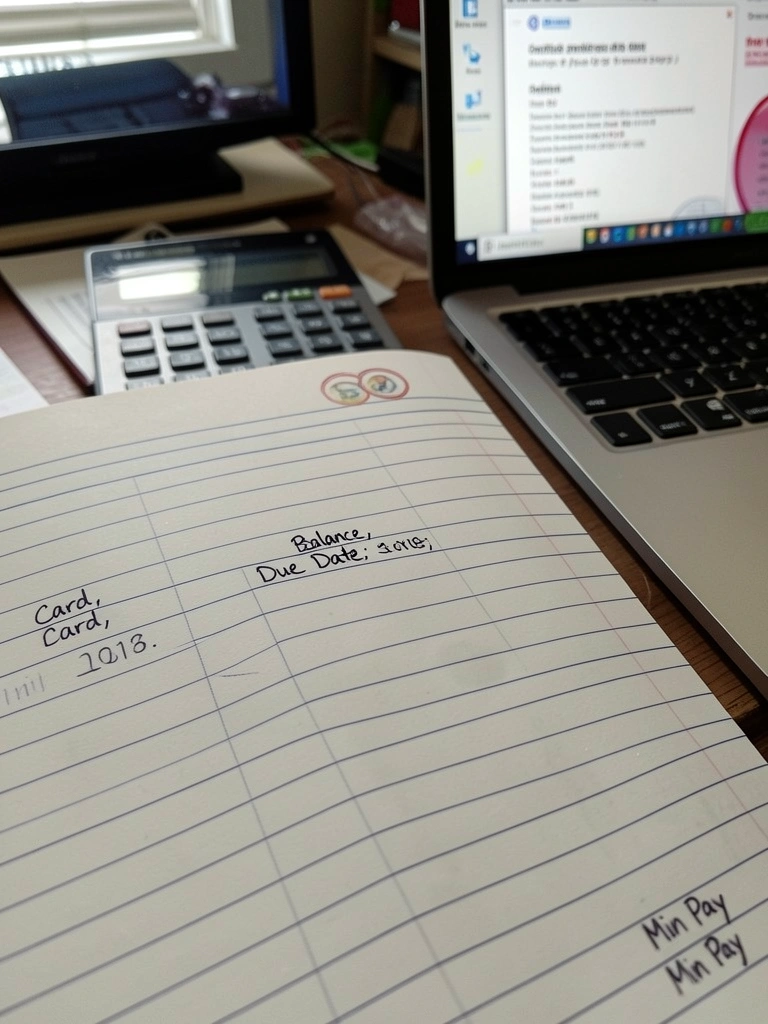

Step 1: List every card, balance, due date, and minimum payment

Start by collecting the facts. Pull the latest statements or online balances for each card and write down the current balance, the due date, and the minimum payment for each.

What changes: you move from guessing to a single snapshot that shows totals and timing. This reduces missed payments and lets you see which balances cost the most over time.

Insight people miss: promotional balances or deferred interest can be on different schedules and need their own line. Mistake to avoid: leaving out small store cards because they seem insignificant; they still affect payment timing and total minimums.

Step 2: Choose a payoff order that matches your goals and motivation

Decide whether to prioritize high-interest balances to save money or small balances to build momentum. Either approach works; the right choice is the one you can stick with.

What changes: your extra payment targets become focused, so every dollar beyond minimums pushes a specific debt toward zero. That focus speeds progress and reduces decision fatigue.

Insight people miss: behavior beats pure math—choose the method that keeps you consistent. Mistake to avoid: flipping methods mid-payoff because of short-term frustration; that slows progress.

Step 3: Free a regular amount in your budget to apply to debt

Look for recurring expenses you can trim or pause and redirect that money to extra card payments. Small, regular cuts (weekly coffee, one streaming plan) add up and create a reliable payment stream.

What changes: your cash flow shifts from discretionary spending to targeted debt reduction. That makes monthly progress predictable and reduces reliance on one-off lump-sum payments.

Insight people miss: temporary, planned sacrifices are easier to maintain than permanent austerity. Mistake to avoid: making a single big payment and not resetting your budget so the extra payment repeats next month.

Step 4: Automate minimums and schedule extra payments where possible

Set autopay for at least each minimum to avoid late fees and hits to your account access. Then schedule a separate automatic transfer or manual calendar reminder for the extra amount aimed at your current target balance.

What changes: you reduce late-payment risk and ensure extra payments happen without relying on memory. That consistency lowers interest accumulation and accelerates payoff.

Insight people miss: some issuers post payments differently; confirm extra payments go toward principal rather than future minimums. Mistake to avoid: assuming one autopay will handle both minimum and extra without verifying how the issuer applies it.

Step 5: Track progress, reallocate freed-up money, and protect the win

Update your list monthly and watch as minimum obligations drop when a card is paid off. When one balance clears, immediately move that card’s old payment into the next target.

What changes: you build momentum through visible wins and increase the amount attacking remaining balances. That compounding effect shortens the overall timeline without new income.

Insight people miss: closing a paid-off account can sometimes hurt available credit and tracking; leave it open unless you have a reason. Mistake to avoid: increasing spending on cards once balances fall; keep the payment discipline in place.

Common mistakes people make with this

You assume small minimums mean less harm. Even small balances create more interest and extra monthly minimums that slow payoff.

You treat payoff as a one-time sprint. It’s steadier when built into your monthly plan so progress doesn’t rely on chance windfalls.

- Skipping documentation of due dates.

- Paying late and relying on grace periods rather than fixing the schedule.

How to know it's working

You see the total outstanding balance fall month to month on your list and statements.

You notice one or two minimum payments disappear and the amount you apply to debt grows without changing income.

Also watch for steady on-time payments and no new card balance growth as simple signals that the plan is holding.

What to do if this doesn't fit your situation

If interest or balances feel overwhelming, consider seeking free credit counseling to review realistic options and negotiate rates or plans.

If your cash flow is inconsistent, use a weekly payment habit and a small buffer in a checking account to cover scheduled autopay obligations.

Keep the process flexible: adjust amounts and cadence based on actual cash available, not a rigid target you can't maintain.

Final Thoughts

Start with the simple list and one repeatable change you can maintain for a month.

Build momentum by automating minimums and directing any freed cash to the next target.

Small, steady wins reduce stress and shrink balances. Check progress monthly and adjust as needed for real, lasting results.